Frequently Asked Questions

- Municipal property taxes are one of the Town’s primary revenue sources and help fund many municipal services residents use every day.

- Property taxes are collected locally by the Town of Ponoka. However, not all taxes remain with the municipality, as a portion must also be collected on behalf of the Province for education, and on behalf of Rimoka Housing Foundation for seniors housing.

- Grants are funding contributions primarily from the provincial or federal government that help municipalities pay for infrastructure projects, community initiatives and municipal services. Some grant funding may be used broadly, while others are dedicated to specific purposes such as roads, utilities, recreation facilities, housing or economic development. Grant funding helps reduce the financial burden on local taxpayers for major projects and investments.

- Reserves are funds the Town of Ponoka sets aside over time to help prepare for future infrastructure maintenance, replacement, emergencies or unexpected financial pressures.

- Debentures are long-term loans municipalities can use to help fund major infrastructure projects such as roads, utilities, recreation facilities and other large capital projects. In Alberta, municipal debentures are regulated through the Province and allow the cost of major projects to be spread over time instead of being paid entirely in a single year. This helps share infrastructure costs between current and future residents who will benefit from the investment.

- The Town of Ponoka owns and operates its own electrical utility. Revenue generated through the utility helps support the operation, maintenance and long-term sustainability of the electrical system.

- Utility fees are user-based charges that help fund services such as water, wastewater, sewer and waste management. Unlike property taxes, utility fees are directly tied to the cost of delivering a specific utility service.

- Additional municipal revenue comes from sources such as recreation user fees and rentals, development permits, business licences and other service charges. These revenues help offset the cost of providing municipal services and programs.

- 76.8% of your municipal property taxes go to the Town of Ponoka;

- 22.5% to the Alberta Government for education taxes. The province distributes the dollars to the public and separate school boards on a per student basis; and

- 0.7% goes to Seniors Housing (which the Town is required to collect on behalf of Rimoka Housing Foundation).

- 74.3% of your municipal property taxes go to the Town of Ponoka;

- 25.2% to the Alberta Government for education taxes. The province distributes the dollars to the public and separate school boards on a per student basis; and

- 0.5% goes to Seniors Housing (which the Town is required to collect on behalf of Rimoka Housing Foundation).

What is a capital budget?

The capital budget pays for maintaining, upgrading and replacing critical infrastructure like roads, sidewalks, utilities and recreation facilities.

The capital budget pays for maintaining, upgrading and replacing critical infrastructure like roads, sidewalks, utilities and recreation facilities.

What is an operating budget?

The operating budget funds all the daily activities of the municipality as it delivers services to the community, such as clean drinking water, waste management, policing, fire protection services, bylaw enforcement, snow and ice control on Town roadways, walking trails, street sweeping, and much more.

The operating budget funds all the daily activities of the municipality as it delivers services to the community, such as clean drinking water, waste management, policing, fire protection services, bylaw enforcement, snow and ice control on Town roadways, walking trails, street sweeping, and much more.

How does the Town of Ponoka fund the operating and capital budgets?

The operating and capital budgets are funded by a number of different sources, including:

The operating and capital budgets are funded by a number of different sources, including:

Property taxes

Grants from the federal and provincial governments

Reserves

Debentures

Revenue from the Town’s electrical utility

Utility fees

Other revenue sources (including recreation user fees, licences, permits and government transfers).

When does the Town of Ponoka approve the budget?

The Town of Ponoka approves an interim budget annually in the fall for the following year. The finalized budget and municipal tax rates are approved in the spring once the Alberta Government sets the final property tax levy for education requisitions and when property assessment values have been updated for the Town of Ponoka.

The Town of Ponoka approves an interim budget annually in the fall for the following year. The finalized budget and municipal tax rates are approved in the spring once the Alberta Government sets the final property tax levy for education requisitions and when property assessment values have been updated for the Town of Ponoka.

What impact does inflation have on my municipal property taxes?

Like households and businesses, municipalities experience rising costs over time. Inflation can increase the cost of fuel, utilities, equipment, construction materials, insurance, contracted services and employee wages.

When municipal costs rise faster than revenues, municipalities may face difficult decisions about service levels, infrastructure investment, taxes and user fees. Keeping tax increases below inflation for extended periods can reduce the Town’s ability to maintain existing infrastructure and services over the long term.

How are my property tax dollars allocated?

For residential property taxes:

For residential property taxes:

For commercial property taxes:

For commercial property taxes:

How does the Town of Ponoka determine what my property taxes will be each year?

Each year, the Town of Ponoka determines how much money it will need to fund the annual budget to pay for all of the services and infrastructure maintenance it provides for the community.

Ponoka Town Council worked hard to keep the 2026 municipal property tax increase at two per cent (which is lower than inflationary cost increases).

Municipal property taxes pay for important municipal services, such as policing and fire services, roadways, parks and recreation, and much more.

These services help keep the Town of Ponoka running and support quality of life in our community.

What is the Alberta Government's education tax?

The Government of Alberta increased its education tax for the Town of Ponoka by 11% for 2026 and 10.8% in 2025.

The Government of Alberta increased its education tax for the Town of Ponoka by 11% for 2026 and 10.8% in 2025.

The education tax is responsible for about a quarter of the increase in residential property taxes in Ponoka this year and more than one third of non-residential property taxes.

This equates to an increase this year of approximately $6.30 per $100,000 of assessed value for residential properties and $13.89 per $100,000 of assessed value for non-residential properties.

Even though the education tax appears on your property tax bill, the amount is decided by the provincial government. The Town of Ponoka is required to collect and send the funds directly to the Alberta Government.

To learn more about the education tax, please click here.

How are my municipal property taxes calculated?

The overall tax rate is calculated by dividing the amount of money required to fund the budget by the total assessed value of all properties in town.

TAX RATE = Total Budget Funding ÷ Total Assessed Property Values

For 2026, residential assessment of properties in the Town of Ponoka increased by $71.4 million, and non-residential assessment increased by $23.4 million for a total overall increase of $94.8 million over the 2025 assessment. The increase in property assessment values is another reason why some property owners in Ponoka may see an increase on their 2026 property tax notice.

Factors that can affect property assessment values are the age of homes, the number of homes in the community, the recent sales of similar properties, and the number and size of businesses in the community.

To calculate the amount of municipal property tax that you pay as a homeowner, the tax rate is multiplied by the assessed value of your property and divided by 1,000.

YOUR PROPERTY TAXES = Tax Rate x Your Property's Assessed Value ÷ 1,000

Please note that the overall increase in your municipal property taxes from year to year is directly related to the annual change in your property’s assessment value.

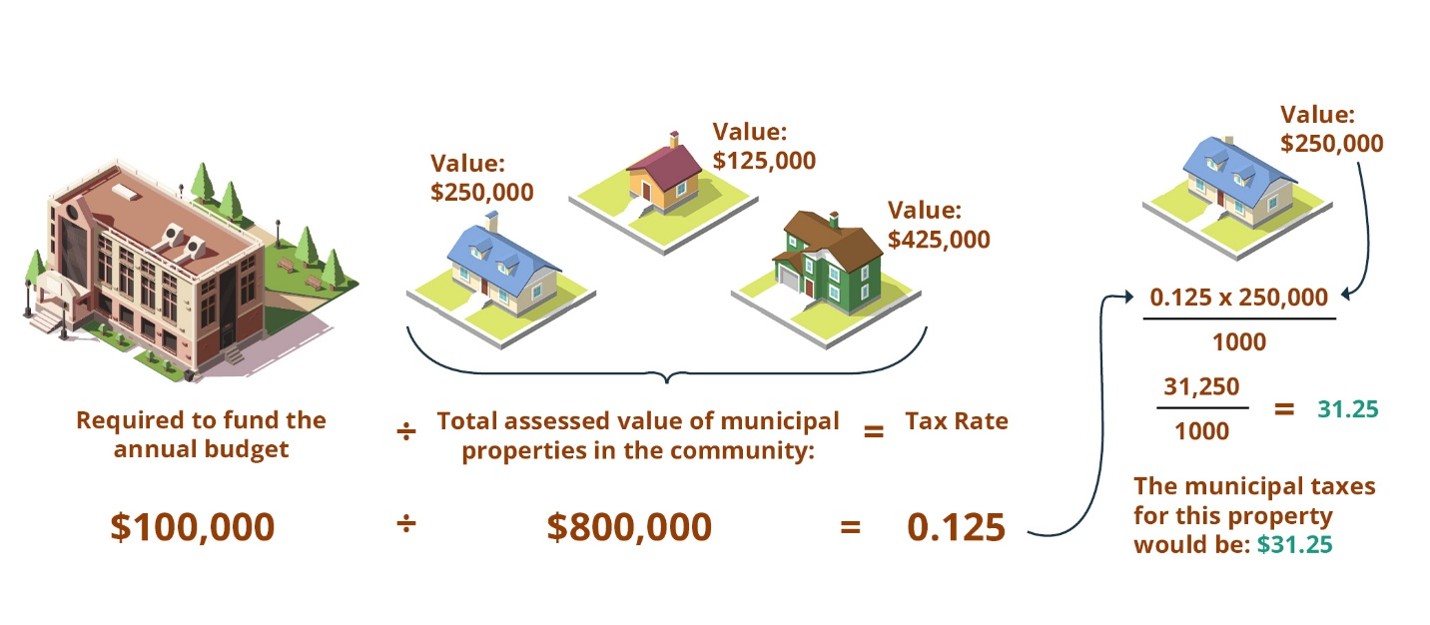

Here is a hypothetical example of how property taxes are determined:

If the Town of Ponoka determines it requires $100,000 to fund the annual budget; and

There are three municipal properties in the community. One is valued at $125,000, the other is valued at $250,000 and the third is valued at $425,000. All three properties total $800,000 in assessed value.

Let's do the math:

$100,000 divided by $800,000 equals a tax rate of 0.125

If your property's assessed value is $250,000, your municipal property taxes would be:

0.125 (tax rate) x $250,000 (assessed property value) ÷ 1,000 = $31.25